Jan Freitag is National Director, Hospitality Analytics for the CoStar Group. He oversees a variety of projects, all charged with the accumulation and interpretation of U.S. lodging data. He is a sought-after public speaker and is frequently quoted in trade publications and the general news media such as The Wall Street Journal, New York Times, Associated Press, Bloomberg and Forbes. ALHI Insider reached out to Jan to share insight on 2023 industry trends for meeting professionals.

With a mild recession on the horizon for 2023, hotel owners and operators are anticipating a year when the ongoing recovery intersects with an economic slowdown. Here are five questions that will be on investors’ and managers’ minds as the hotel industry embarks on the new year.

1. Can Average Daily Rate Growth Continue or Will the Recession Stop Growth?

Average Daily Rate, or ADR, in October was 15% higher than 2021 and 16.8% higher than in 2019. But can this growth continue? The STR forecast answers this question with a resounding yes. The current iteration calls for 1.7% ADR growth in 2023. Looking back over the past 24 months, the upside was strong pricing power. It became obvious quickly that room rate discounts did not induce demand so operators who stuck to their rates are now in a much better position to drive ADR.

How much could a recession matter? It seems like the old adage of two consecutive quarters of GDP decline, which economic observers informally use to quantify a recession, may not be so useful this time around. The U.S. economy is expected to slow in the first two quarters of 2023, but the impact may be much milder than ever before recorded.

The 1.7% ADR growth forecast is below the projected level of inflation, so in real terms ADR will decline, but in nominal terms, it will hit an all-time high. And it’s worth mentioning that ADR growth in a recession is unprecedented.

2. Can Group Recovery Continue?

Companies need culture. Management consultant Peter Drucker famously said: “Culture eats strategy for breakfast.” But in a hybrid or fully remote work environment, getting together with your teammates over video is no way to build culture. Meetings end every hour on the hour and there is no milling around the water cooler, no way to ask deeper questions, no letting conversations take a sharp right turn with “while I have you, I was wondering about … .”

Managers still need to find ways to build team cohesion, and one way to do this is to add new group trips that did not exist in 2019, precisely because everyone was in the office all the time.

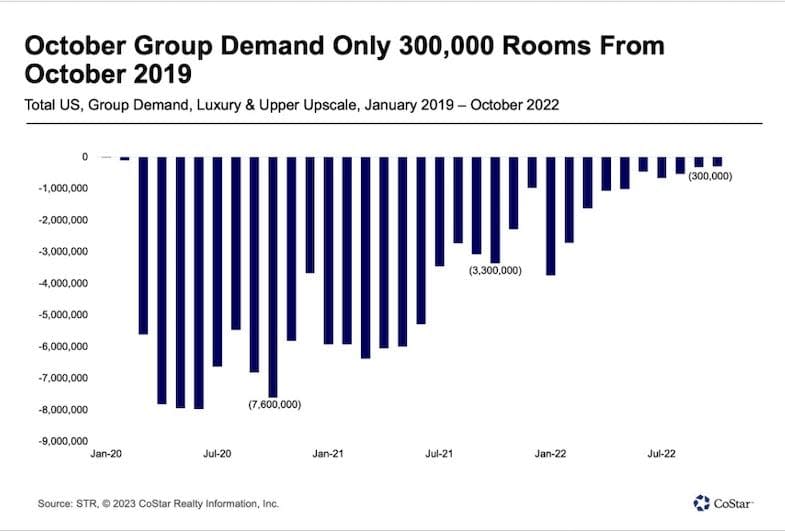

Group demand in October 2022 was only 300,000 room nights below October 2019 demand, and the trajectory points to a full recovery in 2023. A slight slowdown in the beginning of the year could lead to a slowdown in those internal group meetings, but make no mistake: As the economy kicks into a higher gear in the fall, those meetings will happen.

And maybe we will even observe the phenomenon we just lived through in 2022, namely that meetings were postponed from the beginning of the year to the back half of the year, and then very limited meeting space and room blocks are available. Which in turn would translate into even more pricing power and higher rates for those groups.

3. Will Higher Airfares and Flight Delays Impact Corporate and Leisure Demand?

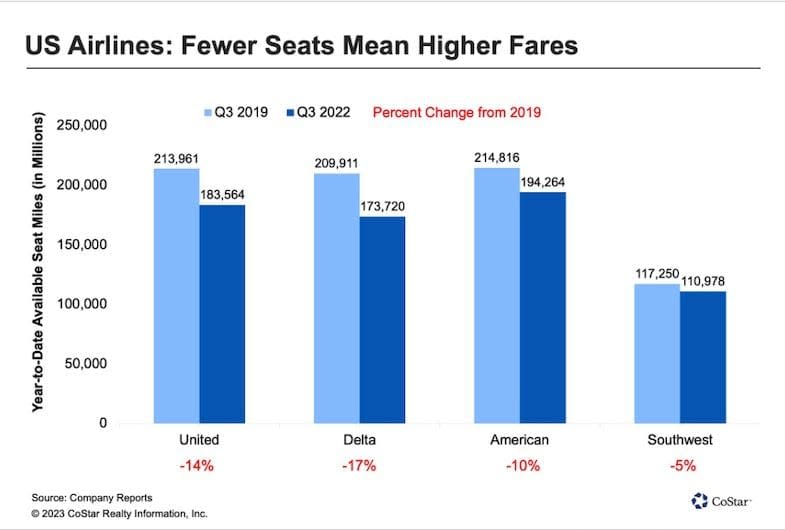

In the good old days of the 2010s, the corporate purchase decision often centered around getting the right hotel room in the right location at the right price. Once that was booked, the way to get to the meeting was often an afterthought — planes and routes were plentiful and airfares, thanks to some low-cost carriers, were reasonable. Not so anymore.

Airfare and access to the right route have become the determining factor in a corporate trip, with midweek hotel availability in many downtown locations almost never a bottleneck. But can travelers actually get to where they want to go? The number of available seat miles is still below, often by double digits, what it was in 2019. Smaller airports have seen their access shrink, in some instances now solely relying on one carrier. But load factors of the domestic carriers are basically back to where they were in 2019. And this demand means that carriers can yield up airfares, sometimes making a trip less likely, especially when it can be substituted with a longer video call. For operators the question then is not what to charge guests once they arrive, but if they will arrive at all.

4. Where Have All the Workers Gone?

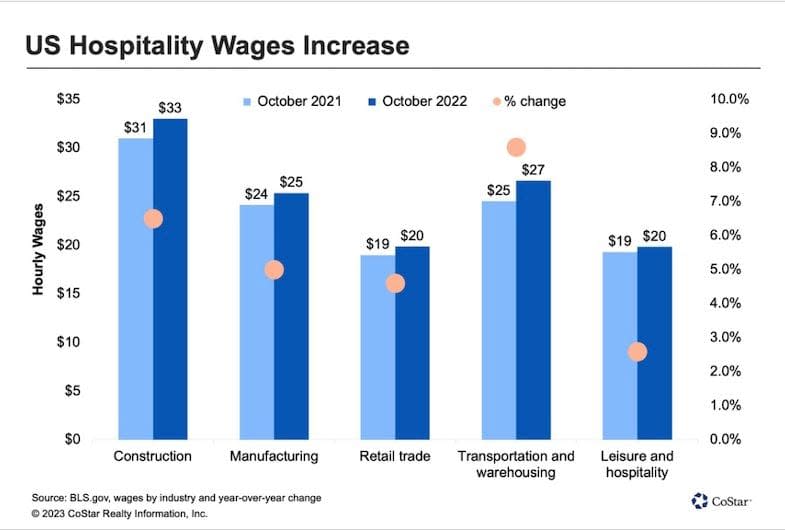

No self-respecting hotel industry conference panel discussion would be complete without the lamentation about the state of the labor market for hourly employees. Bureau of Labor Statistics data tells us that the accommodations industry is still lacking roughly 250,000 jobs compared to the January 2020 staffing count.

When I present to developers or bankers, I often ask: “I have no doubt that you can design the room, finance the room and build the room. But who is going to clean the room?” In some markets that could be the governor of growth.

Much has been written about possible automation and cutting of services, by reducing restaurant hours or stay-over room cleaning. But the conversation also needs to be about wages, access to affordable housing, childcare and immigration. The hotel industry has never had a reputation for paying very well, and the BLS data bears that out.

Higher wages are certainly part of the solution, but so is immigration reform. It's very good to see that the American Hotel & Lodging Association continues its leadership role in this vital area, calling on “Congress to pass comprehensive immigration reform and to pass legislation that strengthens the H-2B and J-1 visa programs.”

The H-2B cap was increased by an additional 66,000 workers at the beginning of Congress’ fiscal year, which is certainly good news for the seasonal resorts in mountains and on beaches. But it’s not enough. Continued lobbying by all partners — owners, management companies, destination marketing organizations and the AHLA — will be necessary to continue to push these agenda items to allow for more workers and continued growth in our industry.

5. Are We Ready to Protect Our Assets, Staff and Guests from Mother Nature?

The National Oceanographic and Atmospheric Administration publishes its Billion Dollar Climate Disaster map each year. The number of claims has been rising, just like the global temperatures, and disasters have impacted lives and properties of hotel operators across the U.S. and around the globe. Owners and managers need to heed the warnings that the next strong weather event is coming; it’s not a question of “if” but “when.”

Operators need to be ahead of the curve with disaster preparedness, not only to protect the well-beings of their guests and staff but also because when the lights go out, hotels are often the shelter of last resort for the surrounding community. Hotels also often become the staging area for first responders who walk into the zones of devastation. This means that emergency generators and emergency drills are no longer just a “nice to have” but a necessity.

When I chat with meeting planners, I often challenge them on their next site visit to not just check out the beautiful pool but also talk through what happens when a weather event occurs. No one wants to envision their guests in danger, but the better the hotel, the better the answer to the question “what happens when something happens?”

Owners are the ones footing the bill for upgrades of equipment, storm drains, shade solutions and generators. Those items are not cheap. But they provide peace of mind to guests and employees alike that they can weather the next storm — which will surely come.